Navigating health insurance often feels like learning a completely new language. Between the complicated acronyms and the ever-changing rules, making the right choice can seem impossible. Many people simply guess when selecting a plan, hoping for the best while fearing the worst. Unfortunately, this guesswork leads millions to overpay for coverage they do not need or face massive bills for care they thought was covered.

The truth is that understanding your health insurance options is one of the most effective ways to protect your finances. By learning the basic mechanics of how these plans work, you can make strategic decisions that keep more money in your bank account. You do not need a degree in finance to master this system. You just need a clear, straightforward breakdown of the facts.

This guide will walk you through everything you need to know to make an informed decision. We will decode the confusing terminology, compare the major plan types, and uncover hidden strategies to lower your healthcare expenses. By the end of this post, you will have the knowledge needed to select the perfect plan and potentially save thousands of dollars every year.

Decoding Health Insurance Terminology

Before you can choose the best plan, you must understand the basic vocabulary. Insurance companies use specific terms to define how costs are shared between you and them. Knowing these definitions will help you calculate your true potential costs.

Premiums

Your premium is the fixed amount you pay every month just to keep your health insurance active. You must pay this amount regardless of whether you visit a doctor or stay perfectly healthy all year. When comparing plans, people often look only at the premium. However, a low premium usually means you will pay more when you actually need medical care.

Deductibles

The deductible is the amount of money you must pay out of your own pocket for healthcare services before your insurance company starts to pay its share. For example, if your plan has a $2,000 deductible, you are responsible for the first $2,000 of your medical bills. Certain preventative services are often covered before you meet this deductible, but for major treatments, you must clear this hurdle first.

Copayments and Coinsurance

Once you meet your deductible, you will usually still share costs with your insurance provider through copayments or coinsurance.

- Copayments (Copays): These are fixed, flat fees you pay for a specific service. You might pay $30 for a primary care visit or $15 for a prescription.

- Coinsurance: This is a percentage of the medical bill you are required to pay. If your coinsurance is 20%, the insurance company pays 80% of the bill, and you pay the remaining 20%.

Out-of-Pocket Maximums

This is the absolute most important number for protecting your finances in a worst-case scenario. The out-of-pocket maximum is the absolute cap on what you will pay for covered services in a single year. Your deductible, copayments, and coinsurance all count toward this limit. Once you hit this maximum, your insurance company covers 100% of your remaining medical bills for the rest of the year.

Comparing the Major Types of Plans

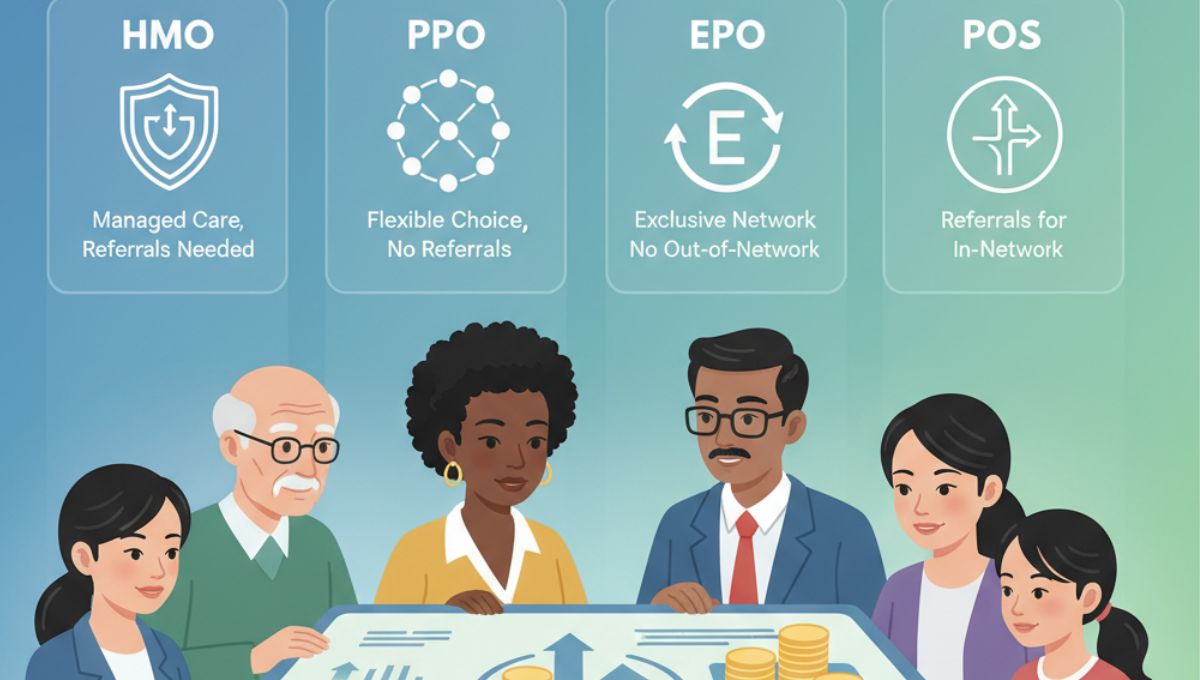

Health insurance plans dictate which doctors you can see and how you receive care. The four most common plan types are HMO, PPO, EPO, and POS. Understanding the differences will help you find the right balance of flexibility and cost.

Health Maintenance Organization (HMO)

HMO plans require you to use a specific, local network of doctors and hospitals. You must choose a Primary Care Physician (PCP) who coordinates all of your care. If you need to see a specialist, like a dermatologist or a cardiologist, you must first get a referral from your PCP.

The main advantage of an HMO is cost. These plans typically offer lower premiums and lower out-of-pocket costs. The downside is the strict lack of flexibility. If you go outside the network (except in a true emergency), the insurance company will not pay anything.

Preferred Provider Organization (PPO)

PPO plans offer a high degree of flexibility. You do not need to choose a Primary Care Physician, and you do not need referrals to see specialists. You can also see doctors outside of your network, though you will pay a higher cost than if you stayed in-network.

This flexibility comes at a price. PPO plans usually have higher monthly premiums and higher out-of-pocket costs compared to HMOs. A PPO is often a good choice if you travel frequently or want the freedom to see any doctor you choose.

Exclusive Provider Organization (EPO)

An EPO is a hybrid between an HMO and a PPO. Like a PPO, you do not need a referral to see a specialist. However, like an HMO, you must stay strictly within the plan’s network. Out-of-network care is not covered at all, except in emergencies. EPOs generally cost less than PPOs but offer less flexibility regarding which doctors you can visit.

Point of Service (POS)

POS plans are another hybrid option. Like an HMO, you must designate a Primary Care Physician and get referrals to see specialists. But like a PPO, you have the option to see out-of-network providers, provided you are willing to pay a higher share of the cost. POS plans are less common today but can be a middle ground for cost and coverage.

Leveraging High-Deductible Health Plans and HSAs

One of the most powerful strategies for healthy individuals to save money is pairing a High-Deductible Health Plan (HDHP) with a Health Savings Account (HSA).

An HDHP is exactly what it sounds like: a health insurance plan with a high deductible and low monthly premiums. While the high deductible can seem intimidating, it unlocks access to an HSA, which is arguably the best tax-advantaged account available in the United States.

The Triple Tax Advantage of HSAs

An HSA is a specialized savings account designed specifically for medical expenses. It offers a unique “triple tax advantage” that no other financial account provides:

- Tax-deductible contributions: The money you put into your HSA reduces your taxable income for the year.

- Tax-free growth: The funds inside your HSA can be invested, and any interest or investment gains grow completely tax-free.

- Tax-free withdrawals: As long as you use the money to pay for qualified medical expenses, you will never pay taxes on the withdrawals.

Unlike a Flexible Spending Account (FSA), the money in an HSA rolls over from year to year. You never lose your funds. If you are generally healthy and have the cash to cover your deductible in an emergency, an HDHP paired with an HSA can build significant long-term wealth while keeping your monthly premiums low.

Strategic Tips for Open Enrollment

Open Enrollment is the small window of time each year when you can choose or change your health insurance plan. Rushing through this process is a costly mistake. Use these strategies to maximize your savings.

Review Your Past Medical Usage

Take an hour to look at your medical bills and claims from the past year. How many times did you visit the doctor? Did you have any emergency room visits? What prescriptions do you take regularly? Calculating your actual spending will give you a baseline to compare different plans.

Anticipate Future Healthcare Needs

Think about the upcoming year. Are you planning to have a baby? Do you have a scheduled surgery? If you know you will have high medical expenses, it usually makes sense to pay a higher monthly premium for a plan with a lower deductible and lower out-of-pocket maximum.

Verify Your Doctor Networks

Insurance networks change every year. Never assume your favorite doctor or local hospital is still in-network just because they were last year. Check the new plan’s provider directory to confirm your doctors are covered before you enroll.

Calculate the Total Estimated Cost

Do not just look at the premium. Calculate the “worst-case scenario” cost by adding the annual premium to the out-of-pocket maximum. Then, calculate your “expected cost” by adding the annual premium to your estimated copays and deductibles based on your past usage. Compare these totals across different plans to see which one truly offers the best value.

Hidden Ways to Lower Your Healthcare Costs

Even after you select the perfect plan, there are everyday strategies you can use to minimize your out-of-pocket expenses.

Take Advantage of Free Preventative Care

Under the Affordable Care Act, most health insurance plans are required to cover certain preventative services at 100%, even if you have not met your deductible. This includes annual physicals, immunizations, and specific screenings like mammograms or colonoscopies. Utilizing these free services can catch health issues early, saving you from expensive treatments down the road.

Utilize Telehealth Services

Many insurance companies now offer robust telehealth programs. Consulting a doctor via video or phone is incredibly convenient and often significantly cheaper than an in-person visit. Telehealth is perfect for minor issues like sinus infections, rashes, or prescription refills. Check your plan’s benefits to see if telehealth copays are lower than standard office visits.

Always Ask for Generic Prescriptions

Prescription drug costs can drain your wallet quickly. Whenever a doctor prescribes a medication, ask if a generic version is available. Generic drugs have the exact same active ingredients as brand-name drugs but cost a fraction of the price. Additionally, use independent comparison tools and pharmacy discount programs to check prices before you fill your prescription at the counter.

Your Annual Health Insurance Checklist

Treating health insurance as a “set it and forget it” expense is a guaranteed way to lose money. Your health changes, networks change, and insurance pricing changes every single year. Use this checklist during your next Open Enrollment period to ensure your coverage aligns with your needs and your budget:

- Evaluate your total medical spending from the previous 12 months.

- List any expected major medical events for the coming year.

- Verify that your preferred doctors, specialists, and hospitals remain in-network.

- Check the plan’s formulary to ensure your routine prescription medications are covered.

- Calculate the total cost (Premiums + Expected Out-of-Pocket costs) for your top three plan choices.

- Consider opening and maxing out a Health Savings Account if you select a High-Deductible Health Plan.

By actively engaging with your health insurance options, you take control of your financial wellbeing. A few hours of research can protect your health and keep thousands of dollars right where they belong—with you.