Best Low-Interest Personal Loans in the USA

Securing a personal loan can feel like navigating a maze of financial jargon, hidden fees, and fluctuating rates. With the economic landscape constantly shifting, borrowing money requires careful consideration and a clear strategy. Whether you need to consolidate high-interest credit card debt, cover an unexpected medical expense, or fund a major home improvement project, finding a loan with the lowest possible interest rate is crucial.

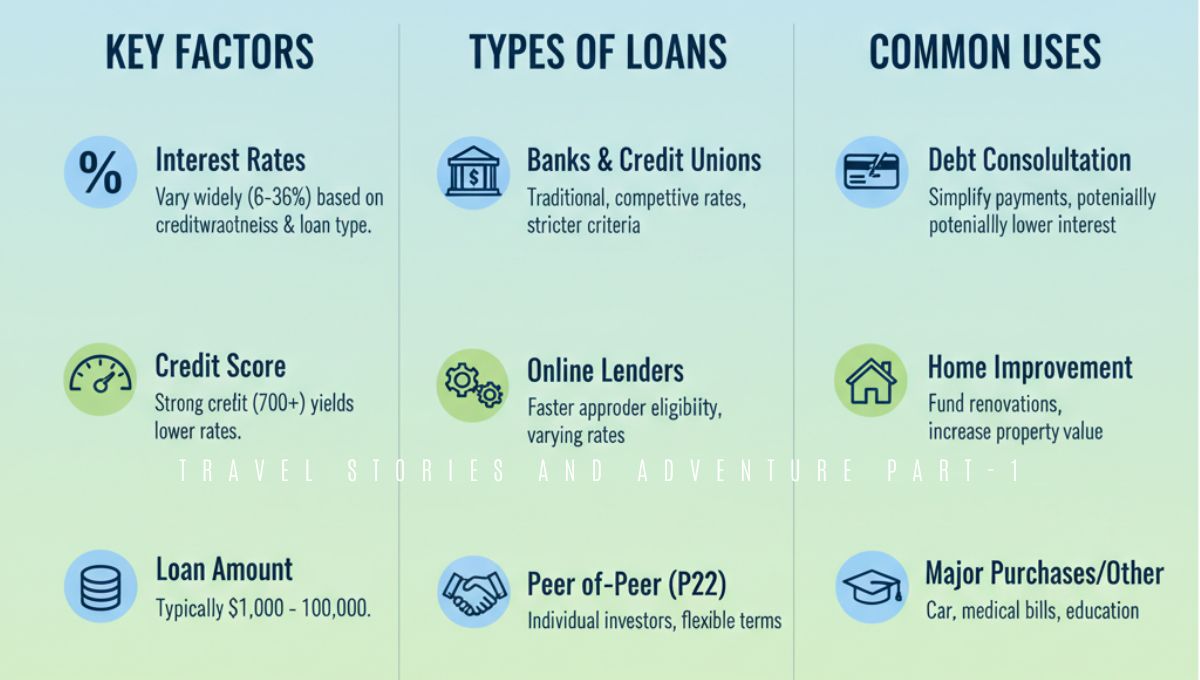

The personal loan market in the USA is highly competitive. Lenders are constantly adjusting their offers to attract reliable borrowers. This competition works to your advantage, provided you know where to look and what to look for. Annual percentage rates (APRs) can range anywhere from the single digits for highly qualified applicants to over 30% for those with riskier credit profiles.

Navigating this environment means understanding your own financial standing before signing any paperwork. By comparing top lenders, knowing how your credit score impacts your options, and avoiding common application pitfalls, you can secure funds without derailing your long-term financial goals. This guide will walk you through the best low-interest personal loan options currently available and show you exactly how to qualify for them.

How Interest Rates Impact Your Total Repayment

Interest rates dictate the true cost of borrowing money. When you take out a personal loan, you are required to pay back the principal amount plus interest. Lenders express this cost as an Annual Percentage Rate (APR), which includes the interest rate along with any upfront fees, such as origination fees.

Even a seemingly small difference in your APR can dramatically alter your total repayment amount. For example, borrowing $20,000 over a five-year term at a 7% APR will cost you around $3,760 in interest. If that same loan carries a 15% APR, your interest charges jump to roughly $8,540. That is a difference of nearly $4,800 out of your pocket.

Understanding this math highlights the importance of shopping around. Lowering your interest rate reduces your monthly payment, making it easier to balance your household budget. It also means you pay off the debt faster, as more of your monthly payment goes toward the principal balance rather than enriching the lender.

Top 5 Lenders for Excellent Credit Scores

Borrowers with excellent credit scores—typically defined as a FICO score of 720 or higher—gain access to the most favorable borrowing terms on the market. Lenders view these individuals as low-risk, rewarding them with single-digit interest rates and zero-fee structures. Here are five of the best options currently available.

1. LightStream

LightStream consistently ranks as a top choice for highly qualified borrowers. They offer highly competitive interest rates and charge no origination fees, late fees, or prepayment penalties. If you agree to set up autopay, they even provide an additional rate discount. LightStream is particularly known for its fast funding process, often depositing money into your account the same day you apply.

2. SoFi

SoFi targets borrowers with strong credit histories and high earning potential. They offer large loan amounts, sometimes up to $100,000, making them ideal for major expenses. SoFi stands out by offering unemployment protection. If you lose your job through no fault of your own, they may temporarily pause your payments and help you find new employment.

3. Marcus by Goldman Sachs

Marcus provides straightforward personal loans with fixed rates and no fees. They reward reliable borrowers with an on-time payment perk. If you make 12 consecutive monthly payments in full and on time, Marcus allows you to defer one payment without accruing extra interest.

4. Discover

Discover extends its reputation for excellent customer service into the personal loan space. They offer flexible repayment terms and do not charge origination fees. Discover also provides a 30-day money-back guarantee. If you change your mind within a month of receiving the funds, you can return the money without paying any interest.

5. American Express

For existing American Express cardholders with excellent credit, Amex offers highly competitive personal loans. The application process is incredibly streamlined since they already have your financial information on file. Funds are typically sent to your bank account quickly, and they charge no origination fees.

Best Low-Interest Options for Fair and Average Credit

Having a less-than-perfect credit score does not exclude you from securing a manageable personal loan. While you may not qualify for rock-bottom rates, several reputable lenders cater specifically to borrowers with fair or average credit profiles (FICO scores between 630 and 689).

Upgrade

Upgrade evaluates more than just your credit score when reviewing your application. They consider your free cash flow and overall financial health. They also offer direct payment to creditors if you are using the loan for debt consolidation, which can help you secure a lower rate.

LendingClub

LendingClub operates as a peer-to-peer lending platform. Investors fund the loans, which allows for more flexible approval criteria. LendingClub is a great option for debt consolidation and offers the ability to apply with a co-borrower, which can significantly improve your chances of approval and lower your rate.

Upstart

Upstart uses an artificial intelligence-driven underwriting model. Instead of relying solely on your FICO score, their algorithm considers your education, employment history, and area of study. This innovative approach helps younger borrowers or those with thin credit files access lower rates than traditional banks might offer.

Benefits of Choosing Credit Unions Versus Traditional National Banks

When searching for the lowest interest rates, many borrowers overlook credit unions in favor of massive national banks. This can be a costly mistake. Credit unions are not-for-profit financial cooperatives owned by their members. This structure allows them to prioritize member benefits over shareholder profits.

Because they operate differently from big banks, credit unions frequently offer lower APRs on personal loans. The National Credit Union Administration (NCUA) even caps the interest rate that federal credit unions can charge on most loans at 18%, providing a crucial safety net for borrowers with lower credit scores.

Furthermore, credit unions tend to have more lenient approval requirements and lower fees. They often take a holistic view of your financial situation, sitting down with you to discuss your income and employment history rather than relying purely on an automated credit check. Institutions like PenFed Credit Union and Navy Federal Credit Union consistently offer some of the most competitive personal loan rates in the country, provided you meet their membership criteria.

Step-by-Step Guide on How to Qualify for the Lowest Possible Rates

Securing a low interest rate requires preparation. Lenders look for specific financial indicators to determine your risk level. Follow these steps to present yourself as an ideal candidate.

1. Check Your Credit Report

Before applying for any loan, pull your credit reports from all three major bureaus (Equifax, Experian, and TransUnion). Check for any errors or fraudulent accounts dragging your score down. Dispute these inaccuracies to give your score a quick boost.

2. Lower Your Debt-to-Income Ratio

Lenders calculate your debt-to-income (DTI) ratio by dividing your total monthly debt payments by your gross monthly income. A high DTI suggests you might struggle to take on new debt. Aim to pay down existing credit card balances to bring your DTI below 36% before applying.

3. Gather Your Documentation

Having your paperwork ready speeds up the approval process. Gather recent pay stubs, W-2 forms, bank statements, and proof of identity. Lenders will use these to verify your income and employment status.

4. Pre-Qualify with Multiple Lenders

Most online lenders allow you to check your rate using a soft credit pull, which does not impact your credit score. Use this feature to gather multiple quotes. Compare the APRs, loan terms, and potential fees side by side.

5. Consider a Co-Signer

If your credit score is borderline, applying with a co-signer who has excellent credit can unlock significantly lower rates. Keep in mind that the co-signer becomes legally responsible for the debt if you fail to make payments.

Common Mistakes to Avoid When Applying for a Personal Loan

Even careful borrowers can make missteps during the application process. Avoiding these common errors will save you money and protect your credit score.

Applying for multiple loans simultaneously is a major red flag. While pre-qualifying uses a soft credit check, formally applying triggers a hard inquiry. Racking up several hard inquiries in a short period damages your credit score and signals to lenders that you are desperate for cash.

Ignoring the fine print regarding fees is another frequent mistake. A loan with a low interest rate might seem attractive until you realize it carries a hefty origination fee. Always calculate the true cost of the loan by focusing on the APR, which includes these upfront costs.

Finally, borrowing more money than you actually need leads to unnecessary interest charges. Stick strictly to your required amount. Every extra dollar you borrow is a dollar you have to pay back with interest.

Master Your Debt and Secure Your Financial Future

Finding the best personal loan with the lowest interest rate requires diligence, research, and a clear understanding of your own financial health. By comparing top-tier lenders, leveraging the benefits of credit unions, and preparing your credit profile before applying, you position yourself for success.

Once you secure your funding, establish a strict repayment plan. Set up automatic payments to ensure you never miss a due date, which protects your credit score and often earns you an interest rate discount. Use the loan as a tool to improve your financial standing, whether that means wiping out high-interest credit card debt or funding a vital home repair. By managing your new loan responsibly, you pave the way for a more secure and prosperous financial future.